Kevin Warsh Hawkish Superstar Has a Stick of Dynamite, and He's Itching to Use It

There are a lot of changes coming to the Fed, just not in interest rates.

He clearly enjoys it. Heck, he might even love it. New Fed Chair Kevin Warsh could barely hold back his excitement at his first post-FOMC press conference as he heaved sticks of dynamite at two decades of monetary policy. He reveled in being an agent of change. Smirking, smiling, and sometimes snarking as he announced what was the most aggressive agenda of any Fed Chair in a generation.

Mr. Warsh is starting his new job at a difficult time, under historic uncertainty, but he clearly could not be more excited about what’s to come. The question is, should the rest of us? I’m not so sure. As laid out in our recent post on what to expect from a Warsh Fed, the need for more optionality through less transparency is one we can, in theory, support. However, central bank communication operates on a spectrum of transparency, and completely eliminating communication practices and upending decades of norms could add even more chaos to what is already a volatile 2026.

There is so much to unpack about the June 2026 press conference and the direction of the Warsh Fed. He clearly took a page from the president’s playbook of ‘come out early and hot’, announcing a set of task forces that aren’t yet fully formed, subtly throwing shade at the last FOMC and Chair, and all but declaring a new dawn at a 113-year-old institution. It’s a bold strategy and one that guarantees that opinions will be formed and changes will be made. Oh, and he was incredibly hawkish — adding another wrinkle to the unexpected mid-June briefing.

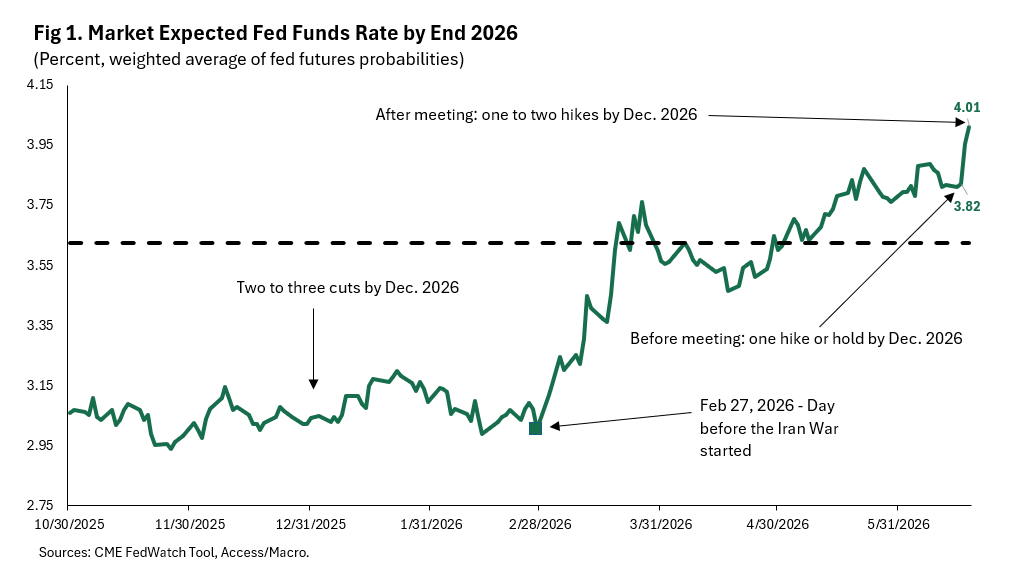

Before we get too far down the rabbit hole of Fed communications, transparency, and task forces, let’s start with the usual stuff. The Fed held rates constant in June. And the FOMC is really concerned about inflation. The SEP, which was probably already outdated by the time it arrived — submissions were made last Friday, and the war “ended” on Sunday afternoon, so the forecasts were likely based on the assumption that it would continue, which would have meant more inflation — had a median expectation of one rate increase by year-end. As Figure 1 shows, that was in line with where markets were going into the meeting.

In a nod to why Warsh doesn’t like the SEP and thus didn’t submit a forecast, markets combined the hawkish vibes of the meeting with the fact that six of the 18 participants expect two raises by the end of 2026 and likely now lean too hawkish. As the figure shows, expectations for the year-end federal funds rate rose by 20 basis points, nearly a full rate increase, in the days following the meeting (the latest data point is end-of-day Thursday, 6/18). That’s too aggressive given that the war is over and energy prices are falling. Expect no change in rates this year, unless, of course, there is another inflationary policy shock.

The other big news for near-term rates was the complete lack of discussion around the employment side of the mandate. As Guy Berger lays out in his latest piece on what to expect this summer from employment revisions, the pattern of disappointing labor market news that has hit during the last two summers and pushed the Fed to cut in the fall of 2024 and 2025 is about to end. The FOMC may be eyeing that same information, which would mean a higher bar for lowering rates, not that the bar was low with the recent inflation data. We don’t expect decent labor market news to push the Fed to increase, but it may be an early signal that the tension between the two halves of the mandate is ending, which would mean a return to “normal economic conditions” where inflationary pressures intensify when the labor market is healthy.

Alright, back to the big news. We’re going to need much more than this post to dig into the task forces and their objectives, the unsettling direction he wants to take data analysis, his views on transparency, communication, and policy, and so much more. For now, you’ll have to be satisfied with some hot takes and views on the near term. Love him or hate him, Mr. Warsh has announced his arrival.

New Vibes for a New World

Before we get started, I have to warn you: there are memes in this post. I’m an old Millennial — no avo toast today, yet — and what we just witnessed was wild. It demands a 2026 response. And what could be more appropriate than a story in pictures and 2000’s movie references?

What Warsh has planned can’t be understood without first discussing the press conference vibes. And oh, what a vibe it was. Normally, these post-FOMC pressers are drab affairs. A statement is read. Questions are stiffly answered. And words are carefully chosen — some might say painfully chosen. Powell was considered a pioneer in Fed communications because he spoke like a normal person and occasionally threw in some good, clean, dad-level jokes. Warsh told us all to hold his beer.

From the very get-go, it was obvious this was going to be a different kind of show. Instead of reading a detailed statement on the FOMC’s assessment of the economy and why the Committee chose to leave rates unchanged in June — it may get buried under the rest of what happened, but the FOMC left rates alone on Wednesday — Mr. Warsh felt the need in his second prepared sentence to let us know that he “listened closely to [his] fellow FOMC members”, and that he “heard a lot of new ideas, new thinking, and genuine interest in moving the Fed forward.”

You might ask yourself, why is this guy (me) making such a big deal about what sounds like a throwaway intro comment? It’s because nobody asked. The desire to reinforce that he (Warsh) listened to others and that they also want to make changes without first telling us the breadth and scope of those changes, and to do so without provocation from those in attendance, was both a nod to one of the biggest questions facing his chairmanship: will he be the kind of Chair that solicits views from his colleagues, or will he be a Greenspan-kind of benevolent dictator — and it was a wink and a nod at the potential vastness of the changes he was gearing up to announce.

Just to compare, Powell, who was already a Governor at the Fed when he became Chair, got right down to business at his press conference. Janet Yellen opened her first press conference with a bland “I appreciate the opportunity” and then launched right into the policy decision and economic assessment. Bernanke started holding press conferences halfway through his tenure, so it may not be the best comparison. His remarks as Fed Chair were at a Semiannual Monetary Policy Report to Congress in February of 2006. Different setting, but he was all business. There weren’t press conferences in the Greenspan era, but he opened his first congressional testimony with a “it’s nice to be here, thank you.”

Warsh went from boyish excitement to be back at the Fed; to I listened to my colleagues, and they want changes; to a list of behaviors he wants to reinforce masquerading as “Fed traditions” he respects; to an announcement that it’s the FOMC’s job to do its job; to a reminder that they are there to do what Congress told them to do: foster price stability and full employment — he barely mentioned the second half of the mandate, more on that later — all in the first 154 words of his prepared remarks.

This portrayal of Warsh’s opening remarks may seem exceptionally nitpicky and unfair. It is not meant to be. These intricacies matter. And they signal both Warsh’s excitement and enthusiasm for his broad agenda, and perhaps some nervousness about his place in Fed history. Rumor has it that Warsh is aware of his place on the Committee and in history. Those may end up being guardrails down the road. His opening remarks were clearly meant to get ahead of them.

None of this is to say that he was shooting from the hip. He was very intentional with his words and clearly arrived on the job with a plan. And he went to great lengths to wrap himself in the cloak of FOMC consensus, something that previous Chairs have also leaned heavily on — at several points during the press conference, he noted that other members supported his views and plans. Consensus still appeared foundational to a Warsh FOMC, at least so far. That is important. It was an open question how far Warsh would try to go it alone. So far, he hasn’t drifted off into the wilderness by his lonesome. His excitement indicates that at least some Committee members are willing to go along for the initial ride. How many is still a very open question.

We’ll find out more in the days and weeks ahead as other Committee members take questions and make public comments. More on this below. But it was clear from the tone and tenor of his remarks, and the smirk on his face, that he feels the wind is at his back. New vibes for a new Fed.

A Hawk Today Doesn’t Mean a Hawk Tomorrow

Here’s a live shot of many of us professional forecasters reevaluating our views on whether Warsh is going to push for rate cuts this summer, two minutes into his opening remarks:

Boy, would some of us like to have that call back — I’m very much including myself. Given the state of inflation, even with the war ending, and the string of recent solid jobs reports, and public comments made by FOMC members, it was obvious that Warsh was walking into a room of people who were not just skeptical of further rate cuts, but were actively debating whether they needed to raise the policy rate this year. However, it was not clear that he would be among them. Warsh had sounded modestly dovish on the near-term path of rates during his congressional hearing, citing productivity as a potential disinflationary force. And everyone knows how the president feels about the current level of rates and his willingness to exert pressure on Fed officials. It seemed likely that Warsh would sound a dovish note amongst a hawkish FOMC. Nope. He came out on Team Hawk, stating:

…the commitment to deliver [on inflation] is strong, unanimous, and unambiguous. And that’s I think an important message we’ve missed for five years, and we’re going to fix that.

He didn’t stop there. Five times he used the phrase “deliver on price stability/objective”. And as my colleague Guy Berger pointed out in his recent piece on the MacroMostly Substack, Warsh didn’t even talk about the employment half of the mandate. Those are clear signs that, at least right now, Warsh is on Team Hawk. Why, and for how long, are still unknown.

While he was quite effusive about his plans to reform the Fed, he refused to give any semblance of a viewpoint on what he believes is driving inflation — understanding the drivers of inflation is apparently an objective of one of the task forces. It’s therefore impossible to know why he was so hawkish. Did Trump misread him (it’s very unlikely Trump didn’t ask about rates and push to have them lowered when he met with Warsh), or does Warsh just expect the inflationary impulse from the Iran War to persist through the summer? Both are plausible. But we’re not going to find out under Warsh’s personal “no forward guidance” framework. He’s committed to not committing, which means we’re entering a golden age for Fed watchers and a period of rising monetary policy uncertainty.

We’re not convinced Mr. Warsh is a full-blown inflation hawk on rate policy. He’s known as an astute observer who can read a room. He walked into an FOMC that is nearly singularly focused on inflation and worried about upcoming price data. He read the room. We expect him to remain focused on the balance sheet and Fed communication rather than the path of near-term rates, and to support rate cuts internally later this year if inflation cools. Mr. Warsh has his eye on bigger things than a 25-basis-point change in interest rate policy. He has a few task forces to run.

Monetary Policy Review Part II: Task Force Edition and Some Hard Feelings

Mr. Warsh was full of surprises on Wednesday afternoon. By far the biggest was his announcement of a group of task forces, each one with a sweeping objective:

FOMC Communication: Warsh has long felt that the Fed, especially relative to other central banks, overcommunicates. As we explained in our outlook piece — What’s Ahead for a Warsh Fed — there is some credence to the view that the new economy needs a new communication strategy that emphasizes optionality, which means less transparency and forward guidance. But the specifics matter, and less doesn’t mean none. Mr. Warsh has a fair bit of leeway here to decide how he and the Committee should engage with the public. Expect this task force to recommend changes to the SEP, particularly removing interest rate forecasts and holding fewer press conferences.

Balance sheet policy: This is Warsh’s biggest bugaboo. He has never really been comfortable with the size of the balance sheet and has strongly opposed expansionary policy when the economy is not in crisis. He wants a smaller balance sheet. Expect this task force to make that recommendation to continue running off the balance sheet. But the FOMC just took up this issue and decided to end the balance sheet runoff (Quantitative Tightening) at the end of last year. There are more than a few Committee members who are concerned about the level of reserves in the system and market liquidity. This is an area of potentially strong disagreement. Watch what Dallas Fed President Lorie Logan has to say as she used to head the Markets Desk — the Fed arm charged with implementing market operations — and she is a well-respected voice on the FOMC. Market operations require an FOMC vote, so Warsh needs to bring a majority of his colleagues on board to move the ball forward on this topic.

Data: His comments on the quality of data and what data should be prioritized were extreme for any policymaker and bordered on revolutionary. He has criticized data, particularly inflation data and how the Fed communicates about it, in the past, but he all but said they’re going to significantly deprioritize agency data, particularly calling out the BLS’s employment data. This had the Trump administration written all over it and has the potential to be the most disruptive and longest-lasting impact of his tenure. The government data has issues — no question. But the FOMC and the world are aware of this, and there are teams of economists working to improve those statistics inside and outside the Fed, and the institution regularly ingests reams of private-sector data. It is very unclear what Warsh hopes to accomplish here, other than to bash official statistics.

Productivity and Jobs: The least controversial and most traditional objective on the list. This sounds similar to existing research teams within the Fed — this issue already has a ton of resources behind it — but it’s one of the biggest economic questions we face. He emphasized several times that the task force won’t be just economists, so it will be interesting to see how its recommendations compare with internal staff assessments. This could be a way for Warsh to circumvent Fed staff views and models without having to replace people internally.

Inflation frameworks: Another one that seems like a bread-and-butter Fed topic on its face. There is a fair argument that the FOMC has spent a lot of time slicing and dicing inflation statistics and that it has thrown up its collective hands a bit at the persistence of inflation. If we’re being generous, he may feel that economists at the Fed need a fresh perspective on both the drivers of price stability and how to communicate about it. A skeptic could view this as a way to minimize the inflationary impact of the administration’s policies. This will be interesting to watch, but we don’t expect the recommendations to be met with a lot of resistance by others on the Committee. Unless, of course, this is a backdoor to deemphasizing elevated inflation as a way to justify lower rates. Given Warsh’s hawkish tone on inflation, we think that is very unlikely.

We’re going to need more details from Mr. Warsh and a lot more space than this post can provide to discuss the implications of all of this. For now, we’re closely monitoring the composition of each task force.

It would have been prime-time TV to see the reaction of those on the FOMC when he announced the formation of the task forces — he likely did it by phone, bilaterally, before the meeting. I’d be willing to wager that it went over three-day-old fish on a hot summer day.

That’s because it’s hard not to view this as anything but a redo of last year’s Monetary Policy Review and an assessment that his colleagues didn’t do their job — that last sentiment was actually peppered throughout the entire press conference:

I've heard a lot of new ideas, new thinking, and genuine interest in moving the Fed forward.

Were members unable to express their views under the old regime? Or did they not feel heard?

But the recent past need not be prologue. I am pleased to report that members of the FOMC are unambiguous and unanimous: This Committee will deliver price stability.

An interesting connection between a regime change and the Fed’s core objective. The word “recent” could be read as an assessment that the last FOMC departed from history on the price stability side of the mandate.

And perhaps the most damning was his view that inflation was a choice.

I've said for years inflation is a choice. You bet it is.

This is just a sampling. You would need two hands to count the number of times that Mr. Warsh threw some subtle shade on the FOMC and his predecessor. Some may argue that Powell started it with his comments at the April FOMC press conference. When asked if he’s confident that Warsh would stand up to political pressure, Powell responded with:

So he testified very strongly to that effect in his hearing, and I'll take him at his word.

Hardly a ringing endorsement. To be fair, Powell had more glowing words for Warsh on this ability to manage the FOMC and Fed credibility, responding to a question with:

And I think Kevin Warsh is actually quite well—he has the capabilities, skills to be very good at that [consensus-building on the FOMC], I would think. So I think—I'm not so worried about that process.

But it’s hard to ignore Powell’s unease over Warsh’s ability to withstand political pressure, nodding to that issue as the reason he’s bucking precedent and staying on the FOMC despite his chairmanship ending:

I want to stay until I—I will stay until it's—I feel it's appropriate for me to leave. And, yes, that [staying on as a “check and balance” to defend Fed independence] is—that is really what is driving this.

This isn’t just palace intrigue. These undercurrents matter immensely for Warsh’s ability to push through reforms, especially with such an ambitious agenda. The Fed is an institution built on norms and culture. And giving a new chair room to flex their agenda is a big one. There will be deference, especially early on, to Warsh and his plans. But, there is a limit to that deference. Expect resistance to big structural changes, particularly if they fly in the face of recent decisions. And as these quotes make clear, he’s not starting from neutral. Powell is not the only FOMC member who has questions about Warsh’s independence from the most invasive administration in decades.

The task forces are likely a subtle acknowledgment that he can’t do what he wants internally, so he’s going to try to outsource some of the arguments and see if he can apply external pressure. But the FOMC is full of big egos and members with a good deal of independence who have some questions about their commitment to central bank independence. Recommendations from an external body won’t change that. In fact, they may make it worse.

It Won’t Be Easy to Silence His Colleagues, Particularly the Presidents

The foundation of the Federal Reserve System, and what differentiates it from other central banks, is the autonomy given to individual FOMC members, particularly Regional Presidents. The autonomy is not boundless, but it is significant. And presidents have been increasingly interested in voicing their own views over the last few decades.

Warsh is not a fan. He wants less chatter by fed officials. He thinks it is creating path dependency with members feeling compelled to remain consistent in their previous forecasts and stifling free discussion as members don’t want to publicly disagree with each other. He laid out his views in his 2025 G30 lecture at the International Monetary Fund:

Fed leaders would be well-served to skip opportunities to share their latest musings…The swivel chair problem, rhetorically waxing and waning with the latest data release, is common and counter-productive.

The very fact that his views are known by the other members will curb some commentary, particularly over the summer. FOMC members are very likely trying to find their bearings in an FOMC under drastic change, and again, they’ll want to provide Warsh with as much latitude as possible. But there will be limits. And not just because they want to exert their own freedom.

Regional Presidents spend a lot of time connecting with communities in their districts. They regularly speak at events and meet with business leaders, bankers, and the broader community, both in person and virtually. And demand for their time is sky high. When I served as chief of staff at the San Francisco Fed in 2019 through the first quarter of 2021, there was a years-long waiting list to have SF Fed President Daly speak at an event. It is similar at every other regional Fed.

Those public events are more than just a chance for Fed officials to voice their opinions. They are a rare opportunity for communities to experience the Federal Reserve in person, and an exceptionally powerful way for an institution with a long history of being hated to show its human side to the American public. They also provide leaders with an opportunity to hear from those not directly involved in the monetary policy process. And Regional Fed Presidents take those events and comments very seriously. There would be a huge uprising if presidents appeared in public less frequently.

But, couldn’t they just say less when they attend an event or say it behind closed doors? Let’s start with the latter. What Fed officials think about the economy, financial markets, and monetary policy is always news. These events are always open to the public or reporters to avoid the optics of a Fed official providing information to only one group. That policy is unlikely to change. Which brings us to: “Why don’t they just say less when they speak?”

This would appear to be an easy route to go for many FOMC members. In fact, some already remain intentionally ambiguous when making public remarks. And there are likely to be more in the months and years ahead. But there are risks to this strategy as well. First, not everyone is good at this, and mistakes are likely to happen, with more significant consequences. If a strategy of ambiguity is widely adopted, it could spotlight misspeaks much more than in the current environment. Imagine a world where all officials speak in ambiguity about the future, and then someone slips up. It would be front-page news, garner more attention than it likely should, and may even push that official to walk back their comments or have someone else on the FOMC come out with a counter-narrative. The public is always searching for insight. Saying less creates a vacuum that occasionally gets filled accidentally. That is exactly the opposite of what Warsh wants.

The second reason widespread ambiguity is risky is that it would cause public frustration and feed the narrative that the Fed is a cabal of powerful people who want to keep the public in the dark. It’s not hard to imagine what that narrative looks like in the volatile and anti-establishment environment of the 2020s.

Officials know all of this and will debate it amongst themselves, and amongst their respective staffs. Some will say less in public. Others, especially over time, are likely to continue to voice their views. That independence is a foundational principle of the Federal Reserve System.

It’s About to Get Wild

This post is over 4k words and is still woefully short of what is needed to understand the direction of the 2026 Fed under Kevin Warsh. We will have a lot more to say going forward. The breadth and pace of changes assure it. But for now, perhaps the best way to sum up Warsh’s first press conference is with this: