FORECAST: Recession Incoming

Even if the Trump Administration avoids tariffs on Canadian and Mexican Imports tomorrow, it's too late. Businesses and consumers have had enough.

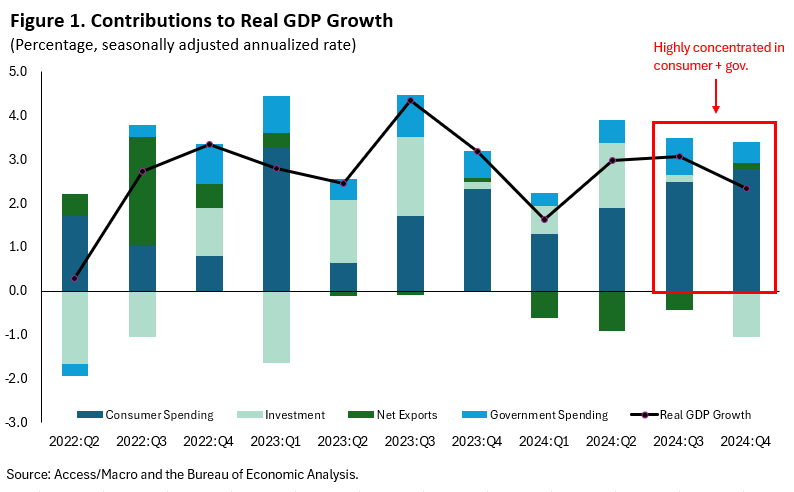

Negative animal spirits have been unleashed. The cumulative effect of rapid and unpredictable cuts to the federal government and the constant threat of tariffs (this was published before Canadian and Mexican tariffs are scheduled to take effect on March 4th) will be too much for businesses and consumers in 2025. Believe the recent consumer sentiment data that households are not pleased and will hunker down to wait out whatever is coming. That’s a problem as growth over the last two quarters has been concentrated in consumer spending, with a dash of positive energy from government purchases, as shown in Figure 1. Those are both about to take a hit. Economy-wide investment already nosedived at the end of the year, and expectations should be for it to remain weak, or even contract further. And don’t look abroad for help. The reduction in imports from a contraction in household spending, and potentially more tariffs, will help Q1 growth (imports are a negative to GDP), but retaliatory tariffs and weaker global growth from chilly trade relations will hurt exports. In short, we’re out of stool legs.

(Email research@accessmacro.com if you’d like to find out how to obtain our February economic and financial forecast suite, which includes a set of detailed projections for many Treasury rates through 2026).

The policy response will sound a lot like crickets: The Fed and federal government probably won’t be able to do much initially to lean against a downturn. Tariffs, or even the threat of tariffs, and continued pressure on some supply chains mean inflationary pressures are here to stay. We won’t get as much of an inflationary bump if the economy contracts, but we also probably won’t get much cooling either. That’s going to hamstring the Fed. Add in that economic data lags real world developments, and the stars are aligned for a late monetary policy response.

The federal government won’t provide much help either. Congress is in the middle of a budget fight, and the mood on the Hill is cost-cutting, not cost-expanding. If the economy turns, we’re not getting another round of stimulus, which could mean a sluggish recovery on the backend.

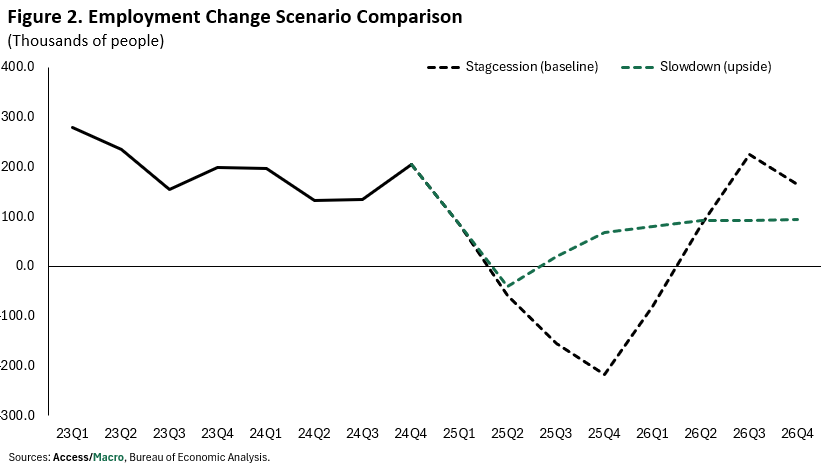

Job losses will spread to the private sector. Our monthly forecasts always include two detailed scenarios. This month, our baseline is for a mild stagcession. We’ve also gamed out an “upside scenario” where household spending slows and investment remains weak, but the economy misses a technical recession—not much of an upside, but it should tell how serious the risks are to our economy. In our baseline scenario of a mild stagcession, cuts in federal employment bleed over to the private sector, leading to significant job losses, as shown in Figure 2. Even without that, we expect employment cuts at federal agencies, and private sector companies that receive federal money, to equate to a full quarter of job losses later this year.

Congress could add insult to injury: The upcoming fiscal fight could hamstring the government’s ability to respond to a recession and apply upward pressure to market interest rates. The debt and deficit will jump even if Congress is able to pass the House budget with substantial government spending cuts, something we view as unlikely. And we expect they’ll decide to borrow more rather than walk back tax cuts if they can’t cut as much spending as they propose. That means the supply of Treasurys will jump over the next few years, weighing on bond prices, which raises bond rates. Talk about swimming upstream as the Fed is trying to cut rates.

Stay ahead of the volatility with our February forecast scenarios. If you’d like to receive our detailed economic and financial projections regularly, email research@accessmacro.com.

Hi, thanks for the insights. I'm not an economist, but I do work with data, and I would like to know what you think: how does this compare to shrinking government spending in the 80s or the recession in 2008?