FORECAST: Comfortably numb

The trade war is on pause, and frankly, we've gotten used to the chaos. That's good news for the economy.

Our baseline forecast shifted back to an economic slowdown, but no recession. As this last weekend proved, we’re still on the trade war roller coaster. But is anyone still afraid? The reduction in the massive 145% tariff rate on Chinese goods down to a still very painful but not end-of-the-world 30% rate was one of the big reasons we’re no longer expecting a recession this year. The other one is that society is adjusting to the chaos. The latest consumer sentiment data showed that consumers are starting to tune out the volatility, although there were still some concerning signs below the surface. And the labor market continues to chug along at a healthy pace. With trade tensions dialed down to simmer, the likelihood of a recession dropped to 45% in our May forecast, and it may be headed lower in the months ahead if actual trade deals start to materialize.

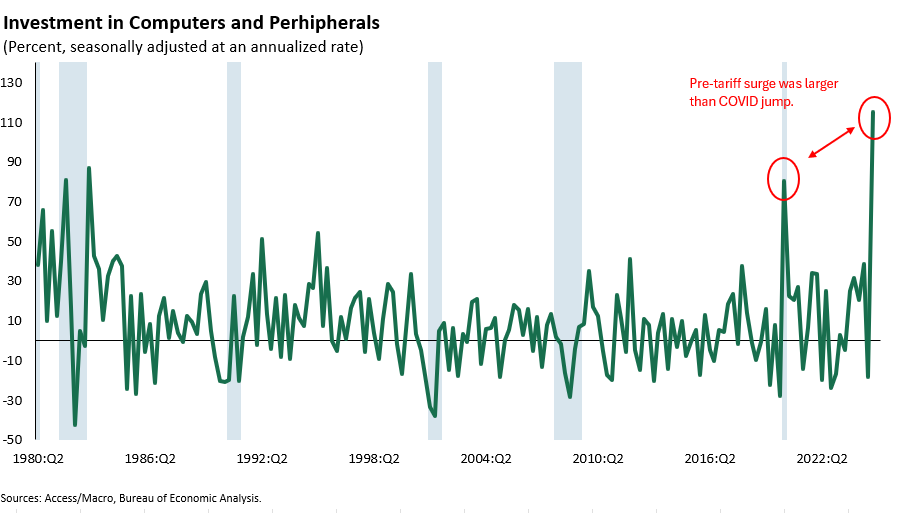

That’s all great news, but we’re not entirely out of the woods. The full impact of the April trade bomb hasn’t arrived yet, suggesting that we’re heading for another economic soft patch in Q2. There was also a metric ton of investment in Q1, much of which was pulled forward as businesses tried to get ahead of tariffs - hello 115% investment in computers and peripherals (see chart below). Expect less investment spending going forward, and maybe less consumer spending. That may lead to another quarter of economic contraction, but it probably won’t lead to a recession unless the economy starts shedding jobs. And we’re not there yet.

(Email research@accessmacro.com to learn how to access our full research suite, which includes detailed economic and financial forecasts built by former Fed insiders).

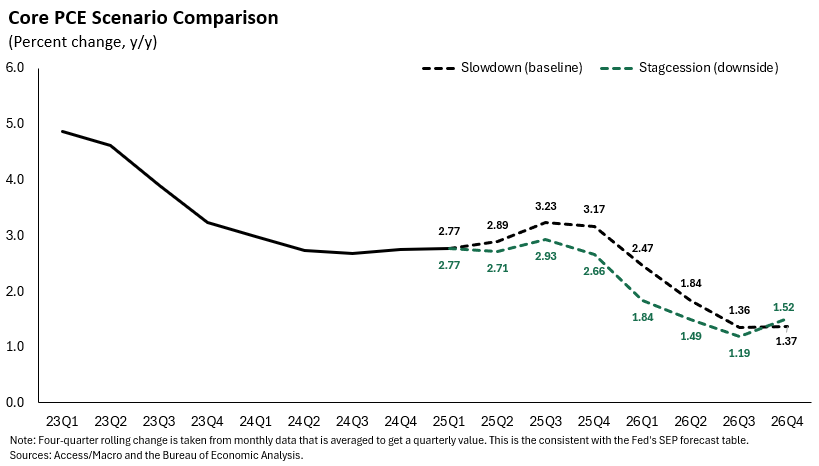

Inflation is a real wild card. Like all things 2025, the inflation data may be breaking tradition. The latest PCE data showed almost no core inflation from February to March. That was right before “Liberation Day,” so we’ll be closely watching the April Personal Income and Outlays report when it comes out later this week. But even that might be too soon to see an inflationary impact. There are many news reports of businesses trying to ride out the tariff wave with only moderate price increases, or eating into corporate profits, so it’s likely that the inflation boost from tariffs won’t arrive until June or July. In any event, the latest news has been disinflationary, which lowered the inflation trajectory in both of our scenarios. Even with that improved forecast, the Fed still might not be able to lower much, if at all, in 2025, if we avoid a recession.

Fed may still be on hold for a while. A lot is going to depend on the next few inflation reports. If we get more disinflation with very low monthly price changes, we’re likely headed for a 25bps cut in September. But that’s optimistic in our view. As we noted above, the tariff impact hasn’t been felt yet. And it’s going to come at a bad time. Just like last year, the 12-month change in core PCE inflation - the Fed’s preferred target - is poised to stall out in the second half of the year. The reasons are technical; they’re called base effects, but unless we get very soft month-over-month readings in the second half of the year, inflation will remain above the Fed’s target in 2025. And that’s with a whole lot of uncertainty around tariffs. If the labor market continues to hold up, and right now it looks like it will, the Fed will be hard pressed to find room to cut until early 2026. Eventually, rates will come down further - economic fundamentals point to another 75bps-100bps in total cuts, but those changes are a way off in a year where chaos reigns. Oh, and we have a potentially very expansionary budget bill set to arrive this summer. Policymakers have their work cut out for them, which unfortunately is the new normal.

Stay ahead of the volatility with our timely economic and financial market analysis. Email research@accessmacro.com to learn how to get our latest research and forecasts.