AI Isn't Causing the World to Implode, but Your Stale Talent Pipeline Might

We published a version of this argument in a Barron's op-ed last week. What follows is the extended director's cut.

The AI headlines continue to push a false dichotomy. According to the people writing the code, it will either force us to toil away for a less-than-benevolent Skynet overlord, or allow us to relax on a beach while soaking in the rays, and our universal basic income.

Overhyping AI is great for stock valuations and FOMO-driven marketing pushes, but it completely obscures the most likely AI outcome: productivity gains for skilled employees, but a persistently sluggish labor market for younger workers.

It’s 2026, so extreme takes are en vogue. But the truth is that tech can be transformational and still not upend society. Living in the infinite set of over-hyped future worlds conceals not only what is likely to happen, but also what businesses should do about it.

The AI Apocalypse Isn’t Coming — But Younger Workers Will Struggle

The early months of 2026 offered a brief reprieve from all the labor market pessimism. January’s employment data showed the economy adding over 100,000 jobs. But the celebration was short-lived. The February data reversed course sharply, and the scary headlines followed: recession fears, AI-displacement horror stories, and just general doom and gloom. The rollercoaster ride continued in the March data, with the preliminary release indicating that the labor market rebounded, adding over 175k jobs at the end of the first quarter.

We’ll forgive you for getting motion sickness. For those of you keeping track, the net balance for employment in Q1 was an average monthly pace of 68k. That is the highest three-month average since April 2025. So clearly good news, right? As one of my mentors used to say, “weeeeeeeellllllll.”

Don’t forget that we’ve had persistent downward revisions to the employment data over the last few years, which means that the current three-month average is likely to fall, maybe by a lot, later this year. Economists love to talk with both hands. Bear with me. So which is it? Is the labor market strong or weak? That’s a challenging question to answer from official government statistics. We need more information to triangulate.

Homebase’s February Main Street Health Report captured something the headline numbers missed: workforce participation held flat in the early part of the year, but hours worked edged up, “signaling stabilization, not expansion.” That distinction matters. A labor market where people are working more hours but fewer new workers are being absorbed looks different from one in collapse. But it also looks different from a healthy one. The latest March report showed even more strength.

The trillion-dollar question is: how much of these changes can we blame on AI? Sure, the world is in a period of intense geopolitical disruption, demographic drag from aging Baby Boomers, and just general policy uncertainty, really on almost every front. Those are all scary in their own right, and even more terrifying when combined. But we’ve all seen Terminator, right? It’s the overlord you have to fear. Not all that other stuff. Or so we’ve been led to believe.

To understand where we’re going, look back at where we’ve been. This isn’t the first time we’ve had panic around technological innovation. In a seminal 2015 paper on automation and employment, MIT economist David Autor documented the consistent tendency of each new wave of technology to generate catastrophic predictions that fail to materialize at scale. He pointed to a 1961 Time magazine headline — “Business: The Automation Jobless” — as an early example. The piece quoted former Pennsylvania Congressman Elmer J. Holland: “One of the greatest problems with automation is not the worker who is fired, but the worker who is not hired.” Sound familiar?

Research actually agrees with Holland, just not at the aggregate, economy-wide level. Autor’s research notes that new technology has never led to a permanent, economy-wide loss in jobs. But it can reshape whole industries. Just look at the manufacturing sector over the last few decades.

Manufacturing employment is down just over 27% from March 2000 to March 2026 — a decline driven by a combination of trade exposure and automation. That kind of industry-level displacement is real and obviously persistent. And we could be entering another cycle. AI almost certainly will hollow out certain white-collar employment. It’s able to do entry-level tasks with ease, and increasingly more accuracy, at a fraction of a fraction of the cost of a full-time newly minted graduate. There’s little chance that future generations of accountants, lawyers, and economists will not be impacted.

We use AI extensively at Access/Macro, for its highest use function - coding. So, what I’m about to say is based not just on trends and historical analysis. It’s coming from the heart of someone who has spent many long days learning how to use it. Despite all its value, AI remains error-prone, constantly disrupted with quality issues, sycophantic, even when you tell it not to be, and lazy, by design. Getting a good answer out of it is an art, not a science. To really maximize its potential, you have to know how to do the work without AI.

Here is where the futurists will jump in, “but, but, but it’s going to get better. And data. And more data. And models. And you don’t know what it can do. And limitless potential. AND LOUD NOISES!!!!” You can almost hear the desperation that every proclamation will drive stock valuations even higher.

Here’s the deal. We’ve had baby AI in the sciences for decades. Yes, the current stuff is souped up and uber-powerful. Yes, it has ingested more data than anything we could have realistically imagined even a decade ago. But, and here’s the thing that really grates the futurists: you can’t ingest enough data or build a model good enough to reliably predict macro events. This isn’t Minority Report. Don’t at me with “this time is different.” Or do, and we’ll have a debate. That’s what comment sections are for. In the meantime, let’s look at what history tells us is most likely to happen and thus, what businesses, banks, and everyone need to do. I’ll say it one more time: To really maximize AI’s potential, you have to know how to do the work without AI.

And there lies the conundrum for younger workers, and ultimately, future talent pipelines. In a world where AI adoption continues to spread and the tech continues to improve, how do young workers stay relevant and in demand? Before we answer that question, let’s take a detour. We’ve talked a lot about the impact on the labor market and what the tech can do. But we haven’t talked about what policymakers can do to help smooth the transition. The answer may be surprising and disheartening.

The Fed’s Get-Out-of-Jail-Free Card They Can’t Control

AI’s implications extend well beyond the labor market. It has the potential to alter the economy’s growth path through higher productivity. A sustained acceleration in productivity would also improve the trajectory of inflation (less) and redefine what “neutral” monetary policy (not damaging interest rate level) actually means. That sounds great for today’s Fed, and all of us! So how does it work?

The mechanism is straightforward. Faster productivity growth raises the economy’s speed limit; we could build more things and provide more services with the same number of workers. More growth with little or no additional labor costs would be disinflationary. Less inflation would allow policymakers to decouple the narrative around higher rates from persistent inflation, focusing on the strength of the economy, not the risks to it. For a Fed currently navigating over five years of uncomfortably high price pressures alongside a softening labor market, that narrative shift would be a welcome reprieve. It would also lead to an economy unburdened by the demand destruction of higher rates, and unshackled by the costs of stubbornly high inflation. Everybody wins. But is this world achievable? Yes, and there are subtle signs that the transformation may already be underway.

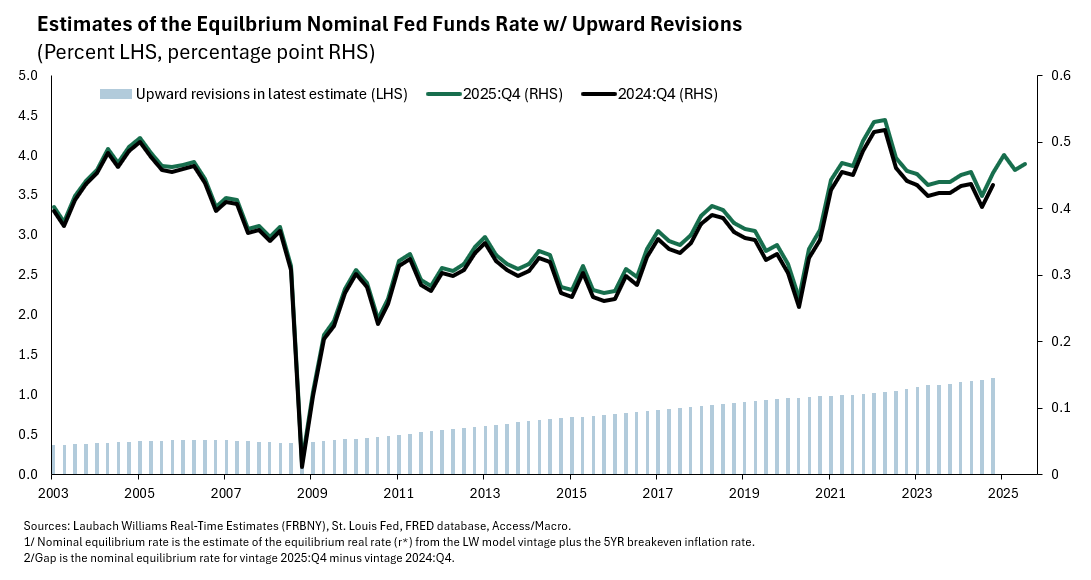

The Laubach-Williams model, created by NY Fed President John Williams and his coauthor Thomas Laubach, is the standard-bearer for estimating the real equilibrium interest rate — the goldilocks inflation-adjusted rate that neither fosters inflationary pressure nor restricts economic growth. Their framework uses advanced filtering techniques to estimate how that rate evolves over time. A stronger potential growth rate is a key driver of a higher neutral rate. That is exactly the world described above. As the figure below shows, the LW model is signaling stronger economic fundamentals and thus, a higher stopping point for the federal funds rate. The lines below show the implied equilibrium nominal interest rate (the model real rate + market inflation expectations), also known as “where the Fed should stop”, in two different time periods. The 2024:Q4 vintage (black line) is below the most recent 2025:Q4 vintage (green line). That means that the latest estimate of the Fed’s stopping point is higher than it was a year ago. But not only that, the bars below the lines — the difference between the two model runs — has been widening for some time. More could be coming with an AI-productivity boom.

Side note: the most recent vintage of that model puts the implied nominal equilibrium rate at 3.75%, placing it at the top of the current federal funds rate target range, which is one reason the Fed is on pause; the other is the persistence of and likely incoming shock to inflation.

But none of that is something the Fed engineered or can influence in the years ahead. What AI can do and how far it can spread are beyond the Fed’s mandate, and more importantly, its capacity. They can’t even do much to offset the “distributional effects” like who wins and loses, or cushion the blow to those who will be negatively impacted, other than running the economy hot, risking more inflation. They’re bystanders in all of this. That might be unsettling to read. It is when I think about it. But it doesn’t mean there’s nothing we can do. In fact, the true power lies with everyday businesses and banks to act in their own self-interest and preserve their talent pipelines. This is one of those moments where what’s good for business is good for society. But it’s going to take money and patience. Two things that are in short supply these days. For those able to stay the course, the potential benefits could be enough to make Scrooge McDuck blush.

Investments in Humans is the Future

AI is democratizing all kinds of work, from database construction and management to accounting to consulting. In the future, the competitive advantage won’t be whether you have AI — everyone will have access to it. The advantage will be whether your company has better harnessed AI to the specific contours of your business, multiplying the power of automation and your workforce. To do that, humans will need to know how to build, manage, and grow those systems to align with company-specific strategies. That will require a workforce trained not only to use AI but, more importantly, to get the job done without it. That’s going to require investment and patience.

But it’s been done before, and with great effect.

AT&T saw the writing on the wall in 2012 and 2013. With the telecommunications industry facing rapid change, the company decided to invest in its current workforce rather than spending to hire people with the right skills on paper. The executives were happy with the results. Bill Blase, AT&T’s Senior EVP of Human Resources at the time, noted the importance of an engaged workforce that is constantly learning to boost customer satisfaction and profits. And CEO Randall Stephenson said that “the difference between growth and obsolescence” will go to those who can “transition their talent at scale as technology changes.” The same will be true over the next decade. The companies that meet the AI revolution by investing in their workforce will be the ones that reap the greatest rewards.

Don’t allow today’s world of immediate gratification, short-term policy plans, the demand for yield, and overpromises about AI’s capabilities to cloud your long-term strategy. Stick to what we know: we’ve seen this kind of rhetoric before during periods of technological innovation, don’t buy into the hype or sell the fear; AI is powerful but ultimately needs continuous skilled human intervention; and the world isn’t ready for either of those. That’s not a cautionary statement. It’s a statement about opportunity.

Tim Mahedy is CEO and Chief Economist at Access/Macro, an independent macroeconomic research firm.

Read the published version in Barron’s

Note: Homebase is an Access/Macro client.